The economic outlook for 2026 started off like a rocket, surprising economists and further solidifying our firm’s view that the economy is on solid footing, and isn’t faltering anytime soon.

Many of you have heard me present, or read here in these pages, about my 53-year business career, and how the tectonic shifts we experienced during that half century dramatically changed the world. Those tectonic events included the invention of the personal computer, cellular telephony and the Internet.

Now a fourth one has crossed my 53-year path: AI. The tailwinds this remarkable invention will blow on our economy portends years of prosperity and dramatically diminished odds of a recession anytime soon.

Jobs Added

The news in January was case in fact: The U.S. economy added 130,000 jobs in January, its strongest growth in over a year, and a sign that the labor market may be shaking off its recent stagnation. As has been reported in the popular business press, January’s robust gains surprised forecasters, blowing far past consensus expectations, while solidifying expectations the Federal Reserve will keep rates on hold for the foreseeable future. The unemployment rate dipped to 4.3% from 4.4% in December, and workers’ wages rose.

The gains were highly concentrated in healthcare and social-assistance fields, which includes jobs like home health aides and residential care workers. Such jobs tend to grow regardless of the economy’s health and have long been an engine of U.S. job growth. This whole phenomenon is driven by the graying of America, as the baby boomers like me require more medical attention as we age.

The picture was much more mixed for white-collar workers, however. Professional and business service firms added tens of thousands of jobs, but 34,000 jobs were lost across the financial activities and information sectors. Elsewhere, manufacturing also added workers for the first time in more than a year.

Paying Attention

We pay careful attention to construction employment, and here the job growth rang the bell. The construction sector grew by 33,000 jobs, mostly on the back of an expanding appetite for new data centers. And this without any appreciable difference in new housing starts, a subset of construction employment that offers the promise of substantial growth when the interest rates drop further and give new home sales a booster shot in the arm.

By way of background, the administration’s dramatic tariffs announcements in 2025 caused companies to put plans on hold, contributing to the weak hiring environment. Now, many of the chief executives are still unclear about what policies will look like this year, but they’re moving forward after shelving many projects.

The January numbers improved on the 48,000 jobs added in December, while surging beyond the 55,000 expected by analysts. The monthly figures are seasonally adjusted. The strongest job growth since December 2024 also marks a turnaround after hiring slowed markedly in 2025, especially after new revisions from the Labor Department show just how tough the market has recently been for job seekers.

But there is a big downside to what should be nothing but good news. The stronger-than-expected jobs report for the month of January is likely to cement the Federal Reserve holds interest rates steady for a while. Our firm believes the jobs report pours cold water on the idea that the Fed could cut rates again before mid-year and will fuel internal debate as to how restrictive policy is and how much slack there is in the labor market.

But with three rate cuts last fall and many Fed officials feeling enough has been done for now to support a job market that looked to be slipping last year, the January report likely reinforces policymakers’ expectations that they’ve done enough for now.

The good job news has had the effect of keeping a lid on interest rates and therefore tamping down housing demand and new home starts. We need to find a balance between job growth and lower interest rates to bring the health of the housing market back to traditional levels.

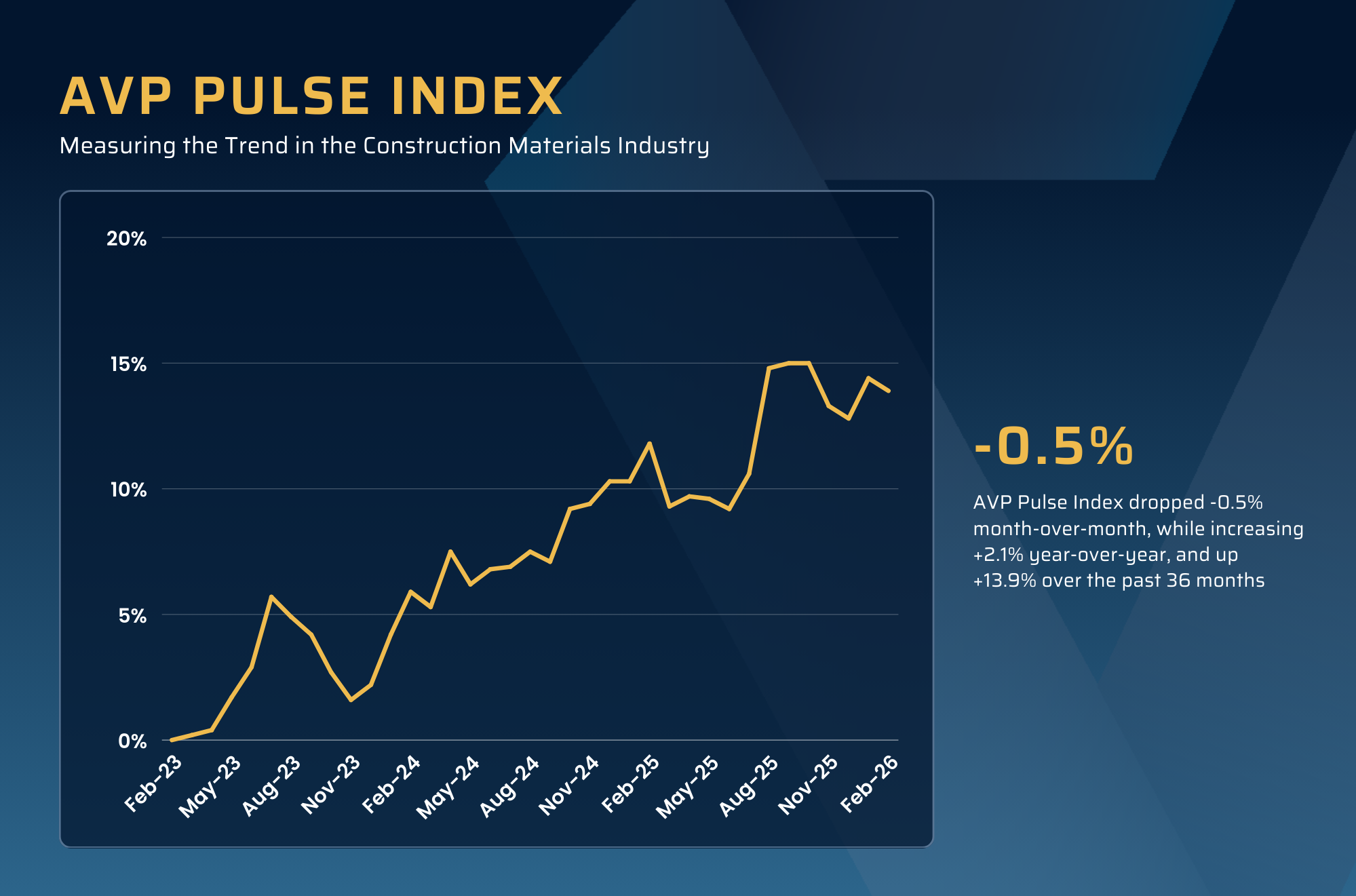

AVP Index

The tight range of movement in the Pulse Index continued last month, with a swing down (-0.5%) month-over-month, but remains positive on both a year-over-year (+2.1%) and rolling 36-month (+13.9%) basis. These percentages closely mirror the general trend and direction over the last several months, with slight movements upwards or downwards but without significant swings.

A big swing to the negative in the Dodge Momentum Index (-6.3%) and the Construction Backlog Indicator (-2.4%) served to significantly downdraft last month’s indicators. Please note that several of the Federal indices that are included in our algorithm were still not available at press time as they are still in catch-up mode from the shutdowns, so once again, the Pulse Index has been driven by a much smaller number of inputs to our model.

It is worth repeating that the AVP Pulse Index is a trend measure, like an arrow, albeit a crooked one; it measures a rolling 36-month period that points up or down depending on the direction of the construction industry.