One thing we can certainly say about the current winds in Washington is that they are blowing the seeds of uncertainty about, as voters and businesses all wonder what the outcome of these never-ending policy changes means for our businesses, and our daily lives. In the 53rd year of my career, I have never known times quite like this.

Now, as we approach the end of the calendar year and opine on the economic outlook for 2026, it is apparent that Washington does not have a monopoly on sowing the seeds of uncertainty and, therefore, guessing what direction we are headed in. A big factor that drives consumer sentiment is the stock market, as the “wealth effect” bolsters confidence in the millions of holders of 401K accounts, which is as important as the stability of consumer prices.

Big Voices. But big voices are predicting very different outcomes for the financial markets in 2026. One major Wall Street firm has become one of the most bullish voices on U.S. stocks, as it predicts a 16% rally for the S&P 500 Index over the next year, underpinned by strong corporate earnings. The bank’s chief U.S. equity strategist expects the benchmark to trade around 7,800 points by the end of 2026. That is among the highest targets from strategists tracked by Bloomberg, and would mean a fourth straight year of double-digit gains for the index.

And further, it expects S&P 500 earnings per share to jump by 17% and 12% in the next two years, respectively, citing improved pricing power for companies, efficiency driven by artificial intelligence, accommodative tax and regulatory policies and stable interest rates.

U.S. stocks are entering the final stretch of a tumultuous year near all-time highs after third-quarter earnings came in much better than expected. Investors remain confident about economic growth despite doubts around high AI valuations, as well as risks from the longest-ever U.S. government shutdown. The S&P 500 has surged 14% so far in 2025, after notching gains exceeding 20% in each of the previous two years.

Different View. But another leading Wall Street bank has a very different view, as it sees markets awash in questionable private credit transactions and unhealthy valuations. Their advice to investors? Load up on cash and stay away from private credit. The bank points to “nosebleed” valuations in the equity market and far too many speculative bets.

The bank is concerned the $1.7 trillion private credit market is engaging in “garbage lending” that could tip global markets into their next meltdown. The collapse of auto lender Tricolor Holdings and car-parts supplier First Brands Group has lent new urgency to what is an oft-repeated narrative, which is that bubbles ultimately burst.

The bank fears the next big crisis in the financial markets is going to be private credit, as it has the same trappings as subprime mortgage repackaging had back in 2006. The bank draws parallels to the inflated AAA ratings of subprime mortgages in the run-up to the financial crisis and warned that private managers may have an unrealistic assessment of the value of their loans. And they claim the industry’s push into retail investors has created the perfect mismatch between a promise of liquidity that is backed by illiquid assets. The risk is that if those funds are hit by redemptions, their inability to sell assets quickly may cause spiraling losses.

The bank also expressed further concerns about the speculative behavior in bets on AI and data centers. Wall Street has been growing more cautious about the huge sums that companies are spending on infrastructure and the hefty prices those at the center of the AI boom command. Shares of chipmaker Nvidia Corp. and the tech-heavy Nasdaq 100 index have both seen downward swoons this fall.

What does this all mean? There is as much uncertainty in the financial markets in 2026 as there is in Washington. Watch that 401K account carefully; I am following the advice of some smart Wall Street guys and staying away from the promise of big returns in the private credit markets, and betting on blue chip companies with steady earnings.

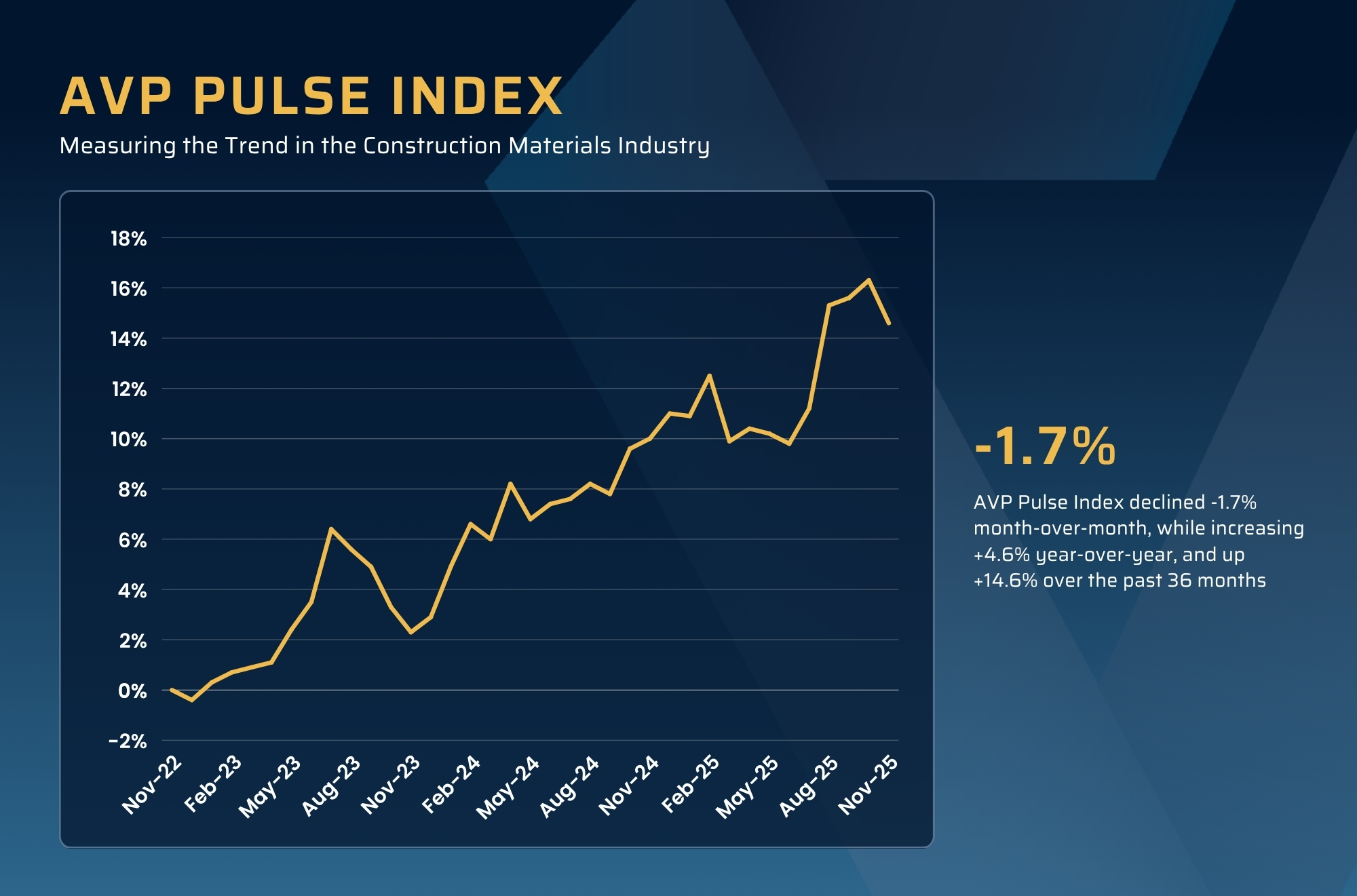

AVP Index. Once again, this month’s pulse index is subject to error, as four of the 10 metrics we process through our algorithm are government-issued figures, and work to compile these numbers has resumed but has yet to be released. Utilizing the remaining measures, we can estimate what an accurate Pulse Index would look like this month. Three of the indicators posted sharp drops, thus reversing last month’s gains. The Index fell -1.7% month-over-month, but is still up a healthy +4.6% year-over-year, and up +14.6% over the past 36 months. While we are missing critical government-issued statistics, we nevertheless saw the Dodge Momentum Index (-7.1%), the Architectural Billings Index (-8.3%), and the Industry Stocks Average Price (-8.2%) all tumble dramatically, posting some of the largest reversals we have witnessed in some time.

It is worth repeating that the AVP Pulse Index is a trend measure, like an arrow, albeit a crooked one; it measures a rolling 36-month period that points up or down depending on the direction of the construction industry. Despite the disruptions brought about by the uncertainty in Washington, we are optimistic this will come to an end eventually.