Allen-Villere Partners Market Analysis

Construction Materials

- The Federal Reserve cut rates three times in late 2025, bringing the Federal Funds target range to 3.50% – 3.75%. The Fed has held rates steady at that level through early 2026 while monitoring inflation and labor market conditions. Current market expectations imply only modest easing in 2026.

- Inflation remained stable in February, with the Consumer Price Index rising 2.4% year-over-year, unchanged from January’s 2.4% rate.

- Key economic variables to monitor in the coming months include the persistence of elevated housing prices, the timing and magnitude of potential Federal Reserve rate cuts, and the economic ripple effects from the ongoing conflict involving Iran.

- The Conference Board Consumer Confidence Index increased by 2.2 points in February to 91.2 from 89.0 in January. The University of Michigan Index of Consumer Sentiment also increased slightly from January (56.4) to February (56.6); however, preliminary March numbers show a reversal to 55.5.

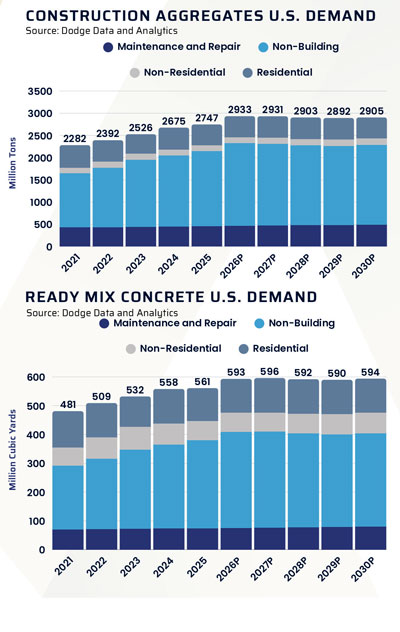

- USGS reported an estimated 870 million tons of construction sand and gravel was produced in the U.S. in 2025, compared with 880 million tons of sand and gravel in 2024.

- The Infrastructure Investment and Jobs Act (IIJA) continues to support demand across the Construction Materials industry. However, the current legislation expires September 30, 2026, meaning Congress will need to pass a new multi-year surface transportation reauthorization bill to maintain federal funding for highways, bridges, and transit projects.

Pierre Villere’s Market Assessment

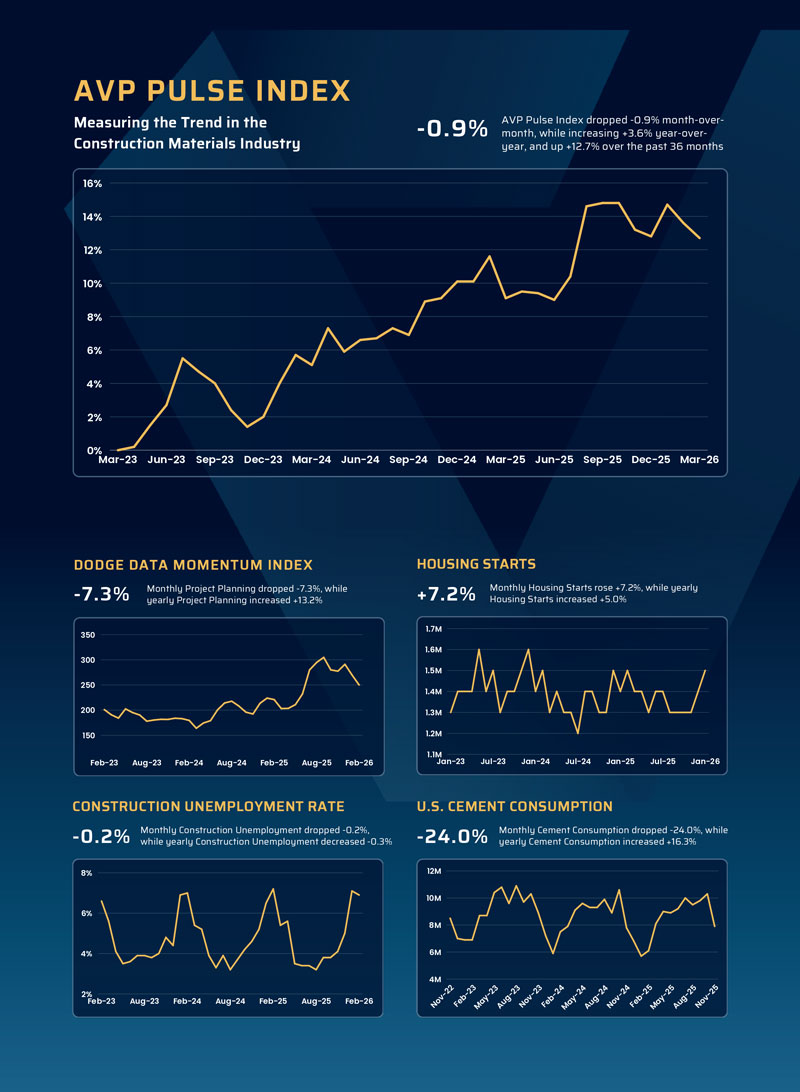

After strengthening earlier in the year, the Index softened this quarter as the AVP Pulse Index declined (-0.9%) month-over-month, though it remains firmly positive on both a year-over-year (+3.6%) and rolling 36-month (+12.7%) basis. The modest decline reflects a mixed set of signals across construction planning, housing sentiment, and financial markets. While long-term momentum across the construction materials industry remains intact, the most recent data suggests a temporary cooling in near-term activity as forward-looking indicators weakened.

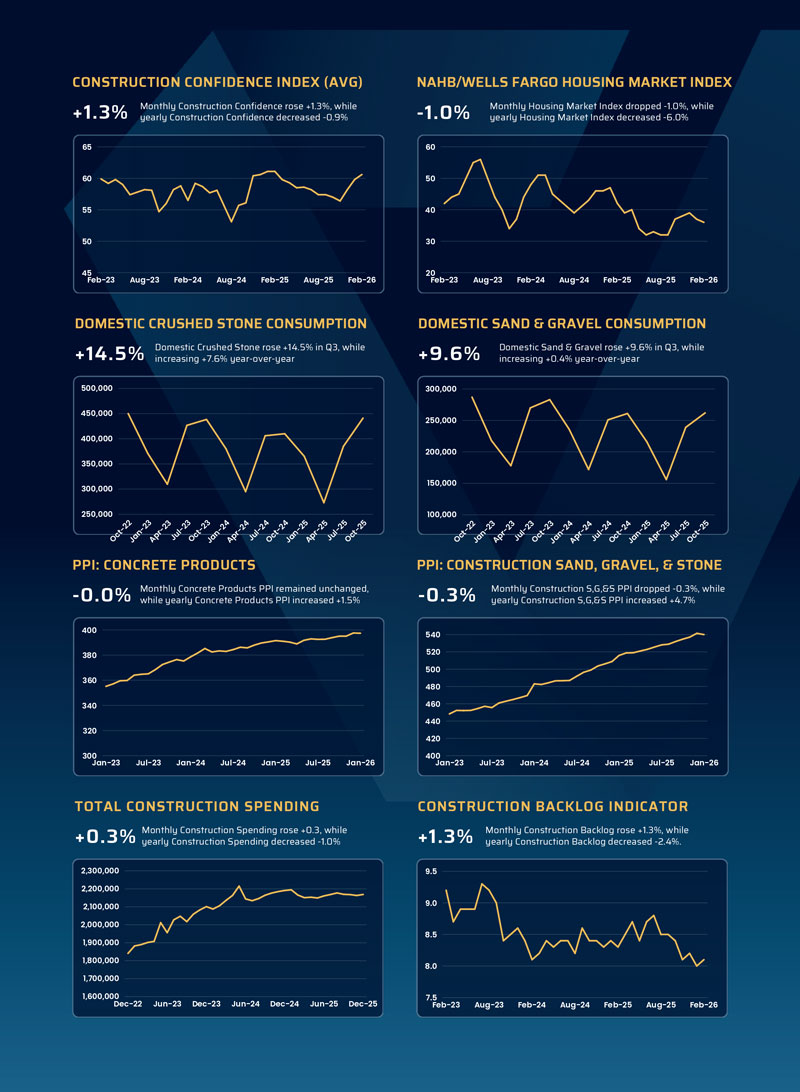

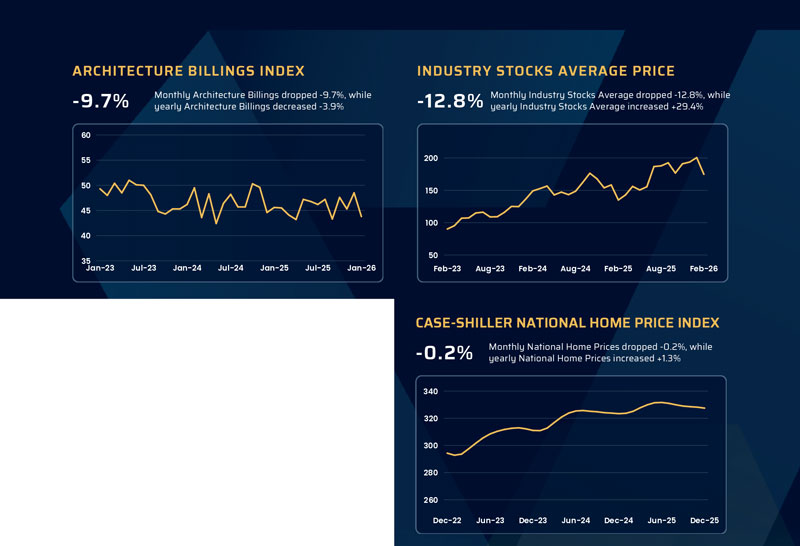

Leading indicators tied to future construction activity showed more pronounced softness during the quarter. The Dodge Data Momentum Index declined (-7.3%) month-over-month, though it remains solidly higher year-over-year (+13.2%), suggesting that longer-term project pipelines remain elevated despite recent volatility. Architecture Billings declined sharply (-9.7% monthly, -3.9% year-over-year), reinforcing evidence that design activity has slowed and fewer new projects are entering the pipeline. Housing sentiment remains fragile, with the NAHB/Wells Fargo Housing Market Index declining (-1.0% monthly, -6.0% year-over-year) as affordability pressures and elevated borrowing costs continue to weigh on buyer demand. However, housing starts rebounded (+7.2% monthly, +5.0% year-over-year), highlighting the uneven nature of the current residential market, where low housing inventory continues to support construction despite weak consumer sentiment.

Despite the pullback in some forward-looking measures, several stabilizing forces remain in place. Total construction spending increased (+0.3% month-over-month), indicating that existing projects continue to progress even as planning activity moderates. Construction backlogs rose modestly (+1.3% monthly), though they remain lower year-over-year (-2.4%), suggesting somewhat tighter visibility ahead for contractors. Labor conditions also remain relatively stable, with the construction unemployment rate declining (-0.2% monthly) and remaining slightly lower year-over-year. Materials pricing was generally stable, with concrete products PPI unchanged month-over-month (+1.5% year-over-year) and construction sand, gravel, and stone prices dipping slightly (-0.3% monthly) but remaining significantly higher year-over-year (+4.7%). Meanwhile, industry stock prices declined sharply (-12.8% monthly) after a strong run, reflecting increased financial market volatility.

Geopolitical developments are also introducing additional uncertainty into the economic outlook. The escalating conflict involving Iran has disrupted shipping through the Strait of Hormuz—through which roughly 20% of global oil supply passes—pushing oil prices close to $100 per barrel and increasing energy market volatility. Higher energy costs could place upward pressure on inflation and construction input costs.

It is worth repeating that the AVP Pulse Index is a trend measure, like an arrow, albeit a crooked one; it measures a rolling 36-month period that points up or down depending on the direction of the construction industry. Despite the recent disruptions, we remain optimistic that current softness will prove temporary and that long-term fundamentals supporting the construction materials industry remain favorable.

About Allen-Villere Partners

Allen-Villere Partners (“AVP”) is the premier mergers & acquisition advisors and valuation services firm to the construction materials industry, focused exclusively on the ready-mixed concrete, construction aggregates, concrete products, and asphalt industries. For over 40 years, AVP has developed a special emphasis on representing the independently owned, middle-markets companies that play such a key role in the competitive landscape of construction materials. With over 60 years in combined experience and highly specialized, industry-specific skills, Allen-Villere Partners has a national reputation for excellence in its client representation.

Track Record

- Valued over 600 companies in this industry over the last 40 years

- Sold over 100 companies in the construction materials industry

- Client relationships in more than 44 states

- Completing deals in this healthy mergers & acquisitions environment