The challenge with writing a monthly column is the lead times required by the publisher, plus the fact that a reader might not see the magazine, or the digital version, until the end of the month. That means a potential span of several weeks, which is a lifetime in this fluid environment, where decisions by Washington can ricochet off consumers and their underlying confidence.

I have written profusely about consumer confidence and the outsized role it plays in the U.S. economy. And as we go to press, that confidence, which we also call sentiment, has plummeted to an all-time low; consumer sentiment plummeted to its lowest level on record due to frustration with price spikes from the U.S.-Israeli war with Iran.

The University of Michigan’s latest consumer survey showed that sentiment declined 11% early that month to a reading of 47.6; remarkably, that is lower than anything seen in the post-World War II era, including during the Great Recession, the pandemic downturn and the historic inflation surge afterward.

As has been widely reported in the popular business press, demographic groups across age, income, and political party all posted setbacks in sentiment, as did every component of the index, reflecting the widespread nature of the April fall.

Improvement Ahead?

However, nearly all of the survey responses were collected before President Trump announced a temporary, and increasingly fragile, ceasefire with Iran. At press time, there is no certainty on where the war will stand, but most economists suggest that sentiment will likely improve after consumers gain confidence that the supply disruptions stemming from the Iran conflict have ended and gas prices start to moderate.

Meanwhile, Americans’ expectations for inflation in the year ahead surged a full percentage point in April to 4.8%, the biggest monthly increase in a year, when Trump unveiled his sweeping “Liberation Day” tariffs. Expectations for inflation over the long term, in the next five to 10 years, saw a more modest uptick, rising to 3.4% from 3.2% in March, the highest level since November.

In a separate report issued in April, the Consumer Price Index surged 0.9% in March, the sharpest monthly increase since 2022, pushing the annual rate to 3.3%, the highest in nearly two years. Economists are all generally of the same mind, warning that rising gas, diesel and airfare prices are already squeezing American households, and this may be only the beginning.

Implications

So what are the practical implications of America’s pessimism? While record-low sentiment itself is troubling, economists care far more about whether it affects consumer spending, which accounts for about two-thirds of the U.S. economy.

U.S. consumers pulling back would put businesses under pressure by lowering their profits, taking a toll on economic growth, and eventually triggering a recession. In February, before the escalation of the Iran war, consumers spent at a solid clip, according to the Commerce Department.

Bouts of pessimism in recent years did not translate into weaker spending, such as during the post-pandemic inflation surge and last year’s tariff spree. And that may remain the case this time around, so long as the U.S. labor market does not deteriorate, most economists say.

While average job growth over the past three months, and smoothing out large monthly swings, remains weak, unemployment also remains historically low at 4.3%. New applications for unemployment benefits also show that companies are holding on to their workers for now.

But investors and economic policymakers broadly believe there is still an uncomfortable risk of unemployment climbing. And if layoffs start to increase, that will likely force Americans to cut back, especially with sentiment down in the dumps.

Economists across the board are warning that negative sentiment is just one of the several ways by which the Iranian conflict will permeate the U.S. economy. At press time, with the conflict unresolved, we expect to see softer readings ahead. Having said that, if a major escalation occurs between this writing and when we publish, expect to see a slow but steady upturn in consumer sentiment and a resumption of the spending that the economy relies on.

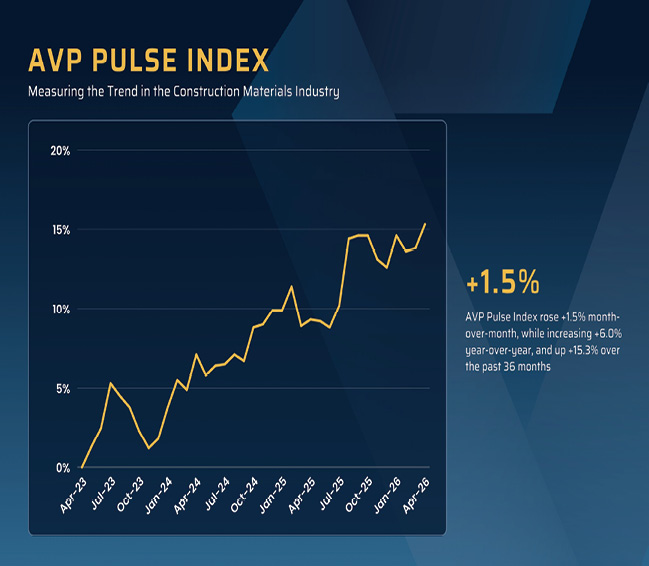

AVP Pulse Index

The Pulse Index broke out of its tight range of the last few months and leaped upwards in most of the indicators. The Index took a swing upwards (+1.5%) month-over-month, and remains strongly positive year-over-year (+6.0%) and on a rolling 36-month basis (+15.3%). These percentages represent some of the strongest gains we have witnessed in many months.

Some very big swings to the positive were in the Architecture Billings Index (+12.8%), the Construction Backlog Indicator (+6.2%), and the positive movement in the Industry Stocks (+9.9%). With the exception of only one indicator that had not been released by the Federal Government at press time, all other government-related indicators were included in this month’s calculations for the first time since the government shutdown.

It is worth repeating that the AVP Pulse Index is a trend measure, like an arrow, albeit a crooked one; it measures a rolling 36-month period that points up or down depending on the direction of the construction industry.